In 2001, Casella Wines decided to enter the American market.

They were a wine producer from Australia.

And CEO John Casella decided that it was time to expand into a bigger market.

But the US wine market was as competitive as it gets.

Hundreds of wine brands from France, Spain, and California filled the shelves at all price points — from low-cost to premium.

Plus Americans preferred beer and other drinks rather than wine.

So if you were to ask a consultant’s opinion about the expansion, he’d tell you that it’s suicide.

But Casella made up his mind.

And they entered the US market under these conditions.

They called the wine Yellow Tail.

The goal was to sell 25,000 cases in the first year.

You know how many they sold?

1,000,000 cases.

And without advertising.

Sailing toward the blue ocean

So how did this happen?

How did Yellow Tail become the leader of a highly competitive market against all odds?

Let’s see.

John Casella knew he had to differentiate to survive in the American market.

So he used his unique insight.

He believed a big group of people didn’t drink wine because it was too complex.

Varieties, vintages, different region names in French…

It was intimidating.

Nobody wanted to understand wine.

They wanted to enjoy a drink.

And that’s why the majority preferred beer or other simple beverages.

So Casella designed Yellow Tail to remove that complexity.

They entered the US market with only two wines.

A white Chardonnay and a red Shiraz.

Both were easy to drink.

And the label on the bottles showed its simplicity.

There were no confusing words.

Only the grape type, Yellow Tail’s name, and its kangaroo.

That simplicity immediately grabbed the attention next to classic wine bottles.

People loved it.

Yellow Tail became a huge success — even more than John Casella imagined.

It became the number one imported wine in the US.

Their revenue reached $350 million in 2021.

In the meantime, strategy professors W. Chan Kim and Renée Mauborgne noticed Yellow Tail’s success pattern in other companies.

Like Cirque du Soleil, Dyson, and Salesforce.

They all entered highly competitive markets as new players.

But managed to win.

So Kim and Mauborgne turned these patterns into a theory in their book Blue Ocean Strategy.

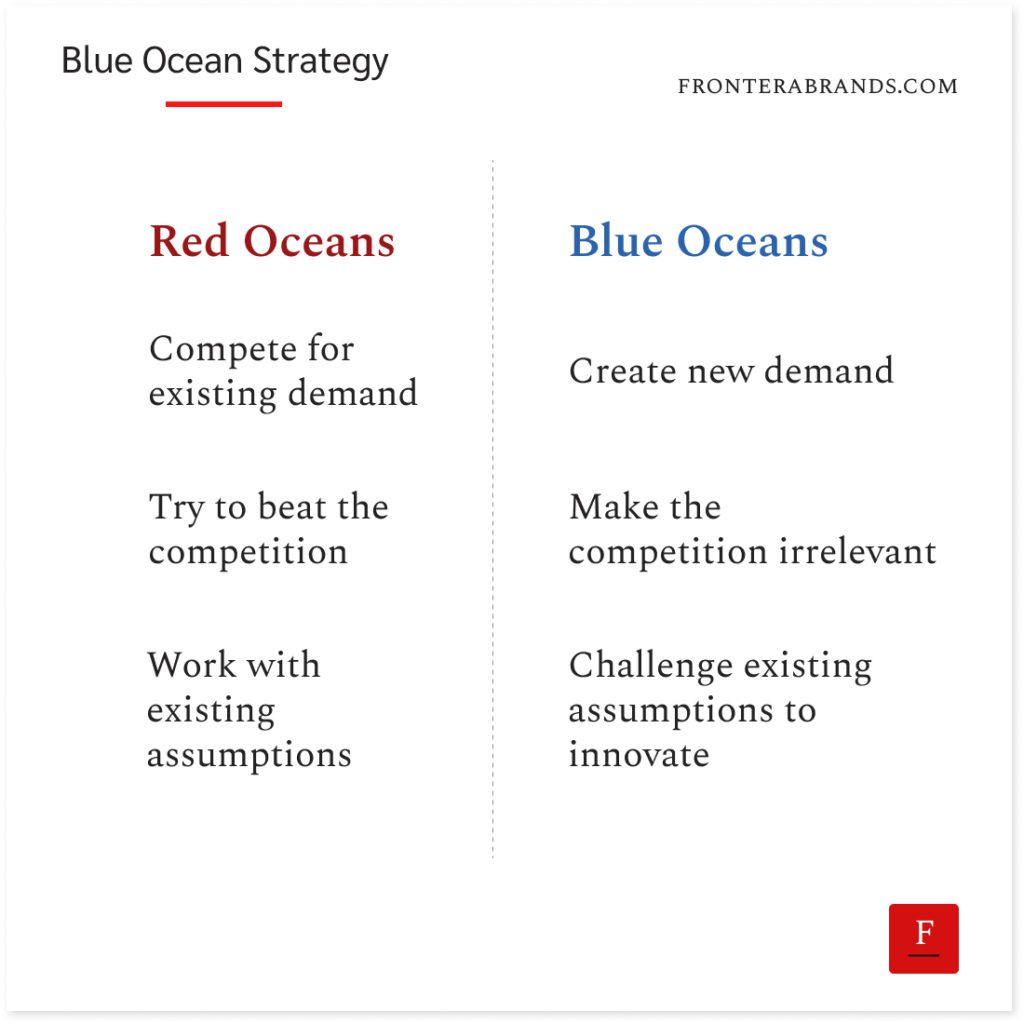

They say there are two types of markets.

Red oceans and blue oceans.

In red oceans, competition is fierce — hence water is bloody.

Many companies try to survive and fail.

But blue oceans are uncontested.

So some players find a blue ocean and create their own market — like Yellow Tail.

Three details to understand the Blue Ocean Strategy better:

- Doesn’t need to disrupt existing players: Blue Ocean Strategy focuses on creating new demand. Yellow Tail’s sales mostly came from new wine drinkers. So existing wine brands didn’t necessarily lose sales.

- Every blue ocean eventually turns red: When somebody discovers a blue ocean, competitors eventually imitate and join the market. But the first player (usually) secures the leader position in the new market by that time.

- Existing players can also find blue oceans: Blue oceans are not always discovered by new players. Nintendo had consoles for years. But with Nintendo Wii, they created a blue ocean by creating new demand for interactive family gaming.

Now the question comes.

How can you create your own blue ocean?

Here are two tips:

1. Start with noncustomers

Sometimes, riches are not in niches.

Yellow Tail went for a broader market than other wine brands.

And they won.

Because they focused on noncustomers.

If Casella had focused on wine buyers; that would mean jumping into the red ocean and competing for the same customers.

But he questioned why noncustomers don’t buy wine.

And removed the barriers to becoming a wine drinker.

Yes, it’s counterintuitive.

But that’s why it allows you to discover untapped markets.

So start with noncustomers to find a blue ocean.

Question why people don’t buy.

You’ll start seeing opportunities nobody else can see.

2. Focus on value innovation

We’ve talked about how Yellow Tail increased the value for customers.

But that was not it.

While doing that, John Casella also reduced costs for his business.

How?

He realized most people didn’t care about the age of the wine.

So he removed the aging process to simplify production.

And Yellow Tail had only two wines — which gave them a big cost advantage against competitors who dealt with dozens.

Kim and Mauborgne called this value innovation.

You aim to increase value while reducing costs.

Their four-step framework to achieve it:

- Eliminate: “Which factors that the industry takes for granted should be eliminated?” Example: Eliminating the wine aging process.

- Reduce: “Which factors should be reduced well below the industry’s standard?” Example: Reducing the wine variety.

- Raise: “Which factors should be raised well above the industry’s standard?” Example: Raising the drinkability of the wine.

- Create: “Which factors that the industry has never offered should be created?” Example: Creating a simple wine label.

As you see, value innovation doesn’t require a tech breakthrough.

But it comes from challenging fundamental assumptions in a market.

So while everybody else is competing on existing assumptions —whether target audience, features, or needs— stop and challenge them.

Make your competition irrelevant to win.

–

Enjoyed this article?

Then you’ll love the How Consultancies Win Newsletter.

Get the “7 Positioning Sins That Cost Consultancy Firms Millions” guide when you join. It’s free.