In early 2002, the Bush administration decided to invade Iraq.

To put the plan into action, they started working on shaping public opinion.

The main argument was Iraq’s “weapons of mass destruction.”

But the press was not convinced.

In one of the news briefings, journalists questioned Secretary of Defense Donald Rumsfeld about the lack of evidence for such weapons.

And he gave his famous answer: “There are unknown unknowns — things we don’t know we don’t know. And if one looks throughout history, these tend to be the difficult ones.”

You know the rest of the story.

One year later, the US invaded Iraq.

The occupation lasted 8 years, and cost many lives and $2 trillion. No weapons of mass destruction were found.

Rumsfeld became the face of the Iraq War failure. People called him “the worst secretary of defense in American history.”

Now, Rumsfeld was wrong about many things.

But his answer in that news briefing contained a useful mental model to understand the degrees of uncertainty.

Our War on Uncertainty

Our brains hate uncertainty.

It’s a source of anxiety.

If your partner or colleague texts you “we need to talk” without giving any details, waiting for that conversation is torture.

Research shows uncertainty is even more stressful than knowing a bad outcome.

And it becomes unbearable when the stakes are high.

Like when you manage a business in a volatile economy.

Or when nobody knew what was going to happen when COVID started.

It’s paralyzing.

So managing uncertainty better is a crucial skill for navigating an uncertain world.

To do that, let’s define uncertainty better using Rumsfeld’s answer.

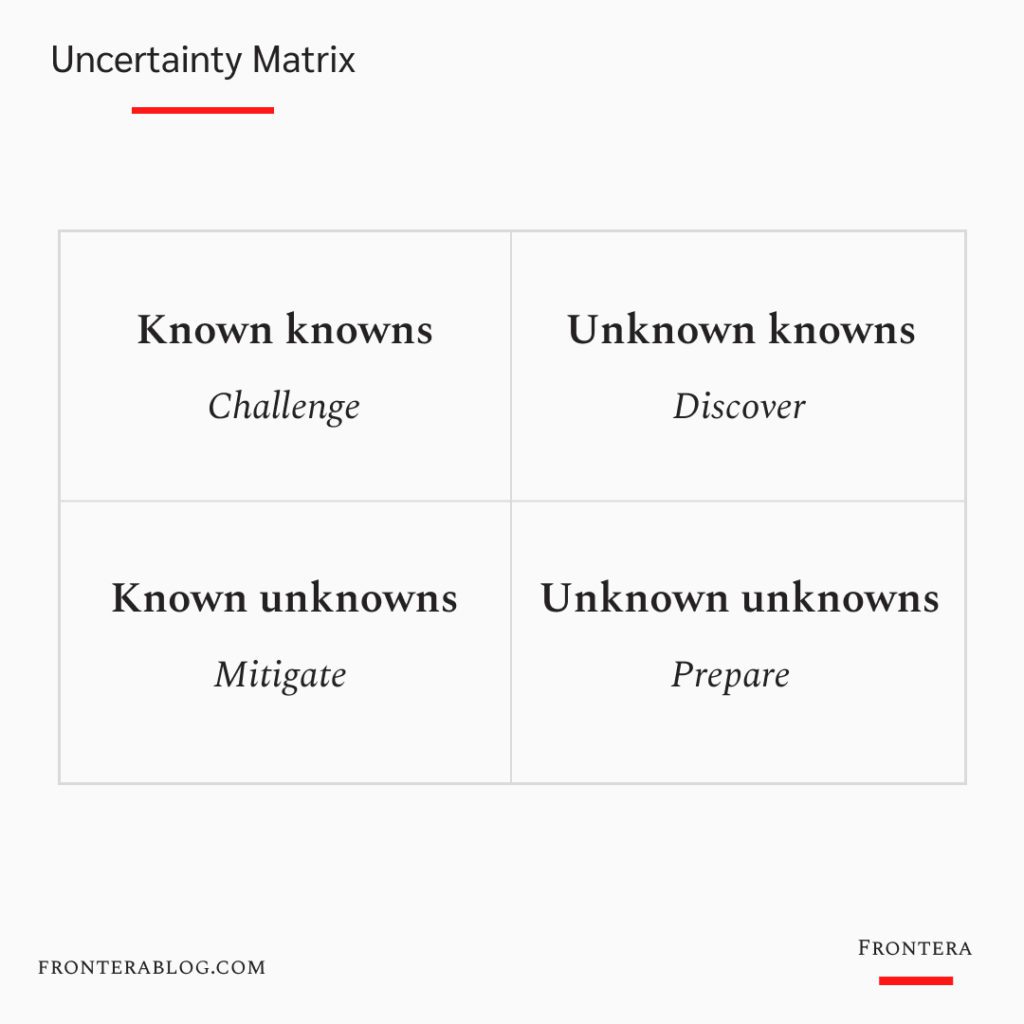

There are four degrees to it:

- Known knowns: When you know something and you are aware that you know it. If you have a product that sells a lot, you know there is demand for it.

- Unknown knowns: Hidden knowledge. You might know how to manage people well and not be aware of it. Or a business might have useful data on customers’ behavior but never turned it into insights.

- Known unknowns: Risks you are aware of. If you leave home during rush hour, you are aware of the risk of traffic and being late. If you start a business, you expect some competitors to copy you.

- Unknown unknowns: Risks you don’t know exist. The real risk. These can cause you the most harm as they catch you unprepared.

Now, the question is what to do with each level.

How To Use Uncertainty Matrix:

1. Challenge known knowns

Nokia had a 50% market share of phones back in 2007.

But its management became complacent.

They thought the working formula would work forever. And never challenged what they knew about what customers wanted.

Even after seeing what a phone can become with the iPhone.

Six years later, their market share went down to 3%.

What’s the lesson here?

Always challenge what you think you know.

And never over-rely on historical data.

2. Discover unknown knowns

I bet it has happened to you before.

You read something and think: “I was aware of this, but never knew it had a name.”

Well, that’s the moment you turn an unknown known into a known known.

So on a personal level, learning more and reflecting are the best ways to discover your hidden knowledge.

But it also exists within organizations.

CEOs make better product decisions when they talk to their customer service team.

Because they uncover hidden knowledge (customer problems, what competitors are doing, etc.) within the organization.

So a little bit of intention to discover hidden knowledge goes a long way.

3. Mitigate known unknowns

This is simple.

When you are aware of a risk, mitigate it.

Insurance is the best example.

4. Prepare for unknown unknowns

This is the fun part.

Some people are never aware of the unknown unknowns.

So for them, risk management ends when they mitigate the known risks.

But the real risk only starts there.

Now, you can uncover some unknown unknowns by war gaming and thinking through scenarios.

Great.

But there will always be more. So to deal with the real risk, don’t try to predict; prepare.

How?

First, add redundancy.

It can be in the form of resources, time, or skills.

Bill Gates kept enough cash to keep Microsoft alive for a year even if they had no revenue.

Probably his advisors thought it was inefficient.

But redundancy makes you sleep well at night.

We all know how companies with efficient supply chains have failed during COVID.

The second thing to prepare for unknown unknowns is to increase your optionality.

Remember the barbell strategy.

Have your options ready.

And be in a position to gain from the unknown.

–

Enjoyed this article?

Then you’ll love the How Consultancies Win Newsletter.

Get the “7 Positioning Sins That Cost Consultancy Firms Millions” guide when you join. It’s free.